Our latest state-of-the-market includes the latest macro economic trends, unparalleled REIT performance data, and a custom transaction scope. Our experts utilize the latest technology stack to penetrate the market and tie these metrics together, procuring the most dynamic assessment in commercial real estate. The proprietary transaction details below deliver real-time informational value to our audience. The report provides a unique vantage point that is non-existent in any other information exchange.

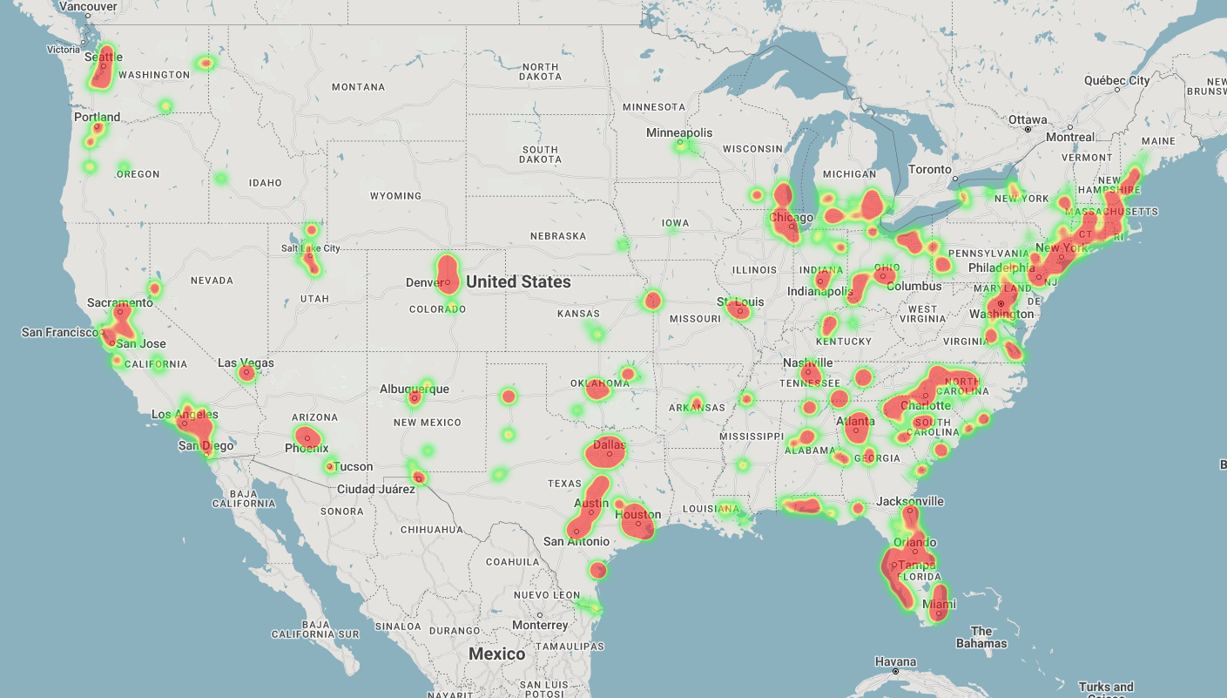

The heat map below visualizes total self-storage sales volume across the United States on a trailing 12-month basis, dating from July 2021 to July 2022.

Our metrics reflect the average time from offering memorandum release to call for offers deadline, average days in due diligence, average days in the closing period, and mean of the earnest deposit percentage for each deal size. This data creates full transparency on the transaction process timeline.

Below, SkyView’s on-market data is broken out from January 2021 to June 2022, categorized by deal size.

The offer data below is broken out by deal type: stabilized, lease-up, and C/O deals. The average number of offers per closing for each deal type is featured to the right of each asset type.

Of the opportunities across the timeline presented in the data below, it is evident that on average, stabilized deals with value-add opportunities such as implementing a conversion or expansion, or adding in tenant insurance programs and competitive market rents, is the most lucrative to buyers in the current climate. Lease-up and deals underway that will be delivered at Certificate of Occupancy (“C/O”) trail just behind the value-add, stabilized opportunities. Demand is present for all self-storage deals; however, the buyer pool remains smaller for the latter two categories in today’s market.

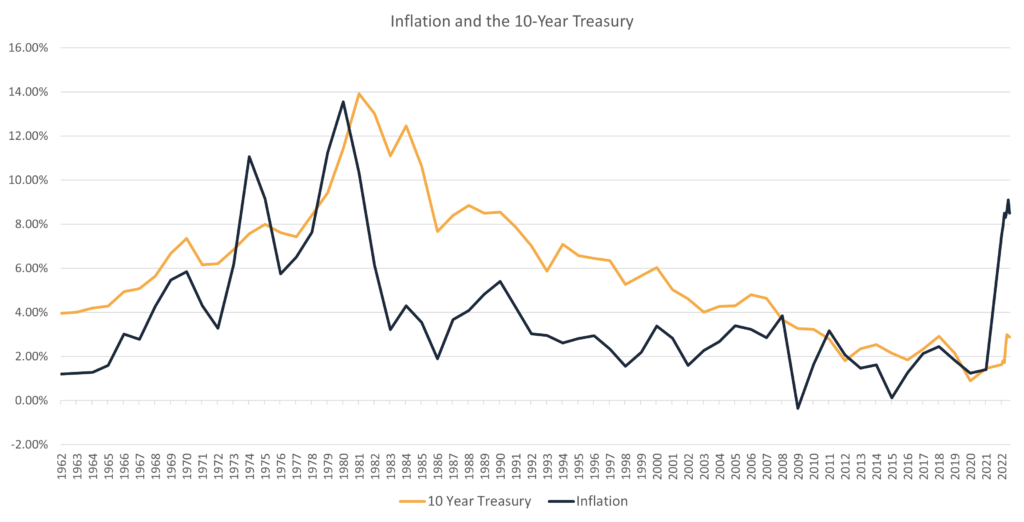

Economic shifts are continuing to impact the market as we enter the back half of 2022. The historic rise of inflation and interest rate hikes in quarter two continue to draw headlines as the industry’s most significant headwinds. These headwinds directly impacted several critical facets of the industry, including future development, rental rates, and cap rates.

A market correction was anticipated after the Federal Reserve went to zero during the pandemic, however, the historical inflation spike in 2022 is still unprecedented.

The visual below demonstrates that our economy is witnessing the highest rate of inflation in 40 years. However, as reflected above in the slight uptick in recent offers, early signs of market stabilization have just begun as inflation trends have decreased, albeit very minimally, in the past 90 days. The recent inflation decrease is reflected in the very far right of the visual below.

Moreover, continued outbreaks of COVID in China and the war in Ukraine have put constraints on the supply chain.

Despite the state of international affairs on the general economy, operating fundamentals for self-storage remain extraordinarily strong. Construction costs remain high, and new supply has been in balance with the demand for self-storage. Positive trends in the market over the last two months will continue to bolster self-storage for the remainder of quarter three, and into quarter four as the economy trends towards stabilization.

Consensus revenue growth and demand is extremely robust. While the widening bid / ask spread between buyers and sellers is in effect, the REITs as well as private equity buyers are still pouring money into the sector with new acquisitions and developments. Revenue increases across the board are attributed to healthy rate increases, justified by strong occupancies and inflationary pressure. Fewer assets have entered the market this year, as rates on construction financing are now in the five percent range and rising. REIT inventory is relatively tight with steady move-in rates, which further justifies demand despite economic pressure. Moreover, achieved rates are up 15-20 percent year-over-year. Consumers and business customers are aggressively seeking space along with more traditional drivers for this time of year, including residential shifts and college move-ins across major markets.

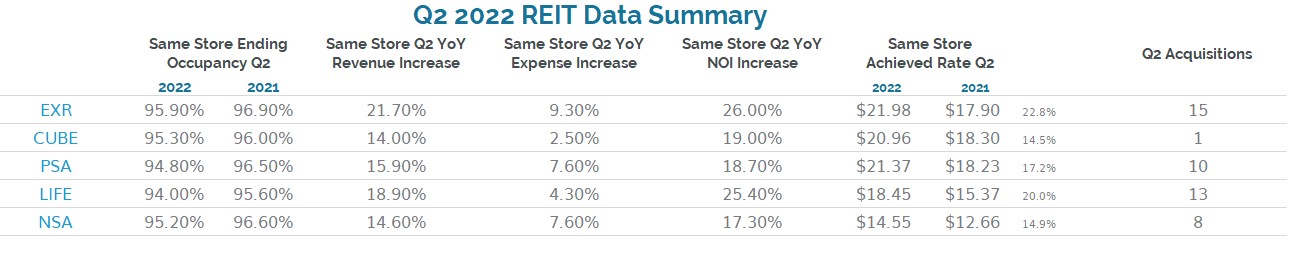

The visual below summarizes the most recent overall REIT performance metrics. Occupancy trends, revenue increases, expense increases, net operating income gains, and rates achieved year-over-year for quarter 2.

The industry is drawing back from the all-time peak of self-storage occupancy in Q2 of 2021 but is positioned still well above historical numbers at 95 percent. Moreover, the year-over-year NOI is on average 20 percent higher than it was last year, demonstrating the resiliency of the asset class, the need for storage space, and robust, ever-increasing fundamentals of the industry. Achieved rates are at an all-time high and are continuing to rise as demand is still very strong. With high occupancies, the REITs can push rates on their in-place tenants to record levels.

*The implied cap rate data indicates the market value of each REIT.

The implied capitalization rate is a culmination of the company value and total debt of each company divided by its NOI.

Implied self-storage REIT cap rates were steadily hovering around four to five percent from 2018 to 2020. Once the pandemic hit, demand increased and asset performance improved. From Q2 of 2020 until Q4 of 2021, cap rates began to trickle down from the mid four percent range to the mid three percent range. Once interest rates began to rapidly increase in the first half of 2022, cap rates began to climb once again, as visualized below.

Achieved Rates and Achieved Occupancies Among REITs are displayed below. The timelines date back to 2018 and reflect rate trends for each quarter.

REIT rate trends remained consistent from Q1 2018 to Q2 2020. The effects of the pandemic are evident as rates began to climb in Q2 of 2020 due to strong demand, yielding all time high rental rates, and occupancies subsequently elevated to their peak as well. The trends are directly correlated as shown below.

As shown by the data below, Q2 continued to represent a consistent busy season for REITs across the board.

Occupancies remained consistent around the 92 percent range from 2018 to Q1 of 2020. The pandemic impact is evident starting in Q2 of 2020, as the demand for storage reached new highs with occupancies growing to 94 percent during the peak of COVID-19. In 2021, occupancies increased even further to all-time highs of 96 percent as displayed below.

As we continue to build our proprietary dataset and technology stack, our analytics will continue to evolve and lead the way. Our unique transaction analysis directly correlates to market conditions.

This next-level combination of informative statistics is geared to help you formulate a strategic business plan for your self-storage asset, regardless of your position. We look forward to leading the way as thought leaders in order to help you achieve your ultimate goals.

Scott Schoettlin

Managing Director

(813) 829 1248

sschoettlin@skyviewadvisors.com

Contributions:

Steven Paul

Senior Financial Analyst

Bryce Josepher

Head of Marketing

Maps Courtesy of Yardi Matrix

Stay up-to-date on the latest self-storage news and insights.

In connection with a potential business transaction concerning The SkyView Pulse | Q2 2022 (the “Transaction”), JDS Real Estate Services, Inc (“Discloser”) may disclose to [COMPANY] (“Recipient”) certain confidential and proprietary information (“Confidential Information”). Confidential Information shall specifically include the fact that the Transaction is being considered. To protect the Confidential Information, the parties hereto mutually agree as follows:

1. Confidential Information may be marked, orally identified as confidential (and subsequently confirmed in writing) or exchanged under circumstances in which it is reasonable to presume it is confidential. Information shall not be deemed Confidential Information if it is: (a) already known to the receiving party, free of restriction when disclosed; (b) is or becomes publicly available through no wrongful act or breach of this Agreement; (c) rightfully received from a third party reasonably known to be without restriction; (d) independently developed without use of or reference to Confidential Information; (e) required to be disclosed by applicable law, regulation, or order of a court of competent jurisdiction; or (f) necessary in the defense of any claim or litigation arising hereunder.

2.Recipient agrees: (a) to regard and preserve as strictly confidential and proprietary, all Confidential Information obtained from Discloser in connection with the Transaction; (b) not, without the prior written consent of Discloser, to disclose the Confidential Information to any person, firm or enterprise, or use the Confidential Information in any manner unrelated to the Transaction; (c) to limit disclosure to their own employees or independent contractors on a “need to know” basis; and (d) upon request, to promptly return or destroy all Confidential Information under their control or in their possession provided, however, Recipient may retain one (1) copy of any Confidential Information, including summaries, compilations or analyses thereof to the extent: (i) required by applicable law or regulation; (ii) required by Recipient’s internal document retention and governance policies; or (iii) would be unreasonably burdensome to destroy (such as any part of the Confidential Information contained in an archived computer system backup). Any Confidential Information retained pursuant to subsections (i), (ii) or (iii) shall continue to be treated as Confidential Information subject to the restrictions set forth in this Agreement, notwithstanding any termination or expiration thereof. The parties hereof agree that money damages would not be a sufficient remedy for any breach of this Agreement, and that Discloser shall be entitled to seek equitable relief as a remedy in addition to all other remedies available at law or in equity. Under no event shall Recipient be liable to Discloser for punitive or consequential damages or lost profits.

3. The Parties agree that references to Recipient shall be meant to apply to only those individuals who are engaged in the Transaction and no other employees, sales associates or officers of Recipient and/or its affiliates

4. This Agreement (a) contains the entire understanding of the parties with respect to the subject matter hereof, (b) may not be changed or modified orally but only by written instrument signed by the parties hereto; (c) is non-assignable and shall expire no sooner than one (1) year from the date of the last disclosure of Confidential Information hereunder; (d) shall be governed by and construed in accordance with the laws of the State of Florida; and (e) may not be strictly construed against either party, each party agreeing that it has participated fully and equally in the preparation of this Agreement.

5. This Agreement may be executed in any number of counterparts, each of which shall be deemed an original and all of which together shall constitute a fully executed agreement, with the same effect and validity as a single, original agreement signed by all of the parties. Facsimile signatures shall have the same validity and effect as original signatures. This Agreement may be signed in any number of counterparts, which together shall constitute a single, fully executed Agreement, as though all of the parties signed the same Agreement

The following information from your profile will be used in the agreement:

THIS NONDISCLOSURE AGREEMENT (this “Agreement”), made as of this 15th day of November, 2024 (the “Effective Date”) [COMPANY], a [COMPANY TYPE], and its affiliates, (“Recipient”), with an address of [ADDRESS], for the benefit of Skyview Advisors LLC (“Discloser”), with an address of 100 N Ashley Dr, Suite 600 | Tampa, FL 33602 (collectively, Recipient and Discloser are the “Parties”).

WHEREAS, Recipient been advised that Discloser is acting as the exclusive agent to the owner of the property known as The SkyView Pulse | Q2 2022 and located at (the “Property”);

WHEREAS, Discloser is willing to provide to Recipient the certain information pursuant to the terms set forth herein in order to facilitate a potential transaction between Recipient and the owner to the Property in connection with the Property (the “Transaction”);

WHEREAS, subject to full execution of this Agreement by all Parties, the Discloser intends to provide Recipient with certain proprietary and confidential information as determined by Discloser relating to the Transaction. All of the information listed above, and any other reports, materials or information obtained by Recipient and its affiliates and/or their respective employees, attorneys or accountants (collectively, “Representatives”), without regard to whether a court of law would deem such materials confidential or privileged, are collectively referred to as the “Confidential Information.”

NOW, THEREFORE, in consideration of the undertakings, and subject to the terms and conditions set forth in this Agreement, as a condition to the disclosure by Discloser to Recipient of any Confidential Information, the Parties agree as follows:

1. Confidentiality and Nondisclosure

(a) Recipient agrees that it will not, directly or indirectly, without the prior written consent of Discloser, disclose or authorize or permit anyone under its direction to disclose to anyone any of such Confidential Information; provided, however, that Recipient may disclose the Confidential Information to those of its Representatives who are engaged to assist in the review of the Transaction if Recipient provides its Representatives with a copy of this Agreement and informs its Representatives of its obligations hereunder. Recipient agrees that neither it nor the Representatives will use any Confidential Information other than in connection with the evaluation of the Transaction.

(b) Recipient and its Representatives will not, without the prior written consent of Discloser, disclose to any person the fact that the Confidential Information exists or has been made available, that Recipient is considering the Transaction, or that discussions or negotiations are taking or have taken place concerning the Transaction, or any term, condition or other fact relating to the Transaction or such discussions or negotiations, including without limitation, the status thereof.

(c) Confidential Information shall not include information which has come within the public domain through no fault or action by Recipient or information which is obtained after the Effective Date by Recipient from any third party which is lawfully in possession of such information and not in violation of any contractual or legal obligation with respect to such information; provided that, with respect to any of the foregoing exceptions, Recipient will, within ten (10) business days of any request therefor by Discloser, provide Discloser with satisfactory written evidence that such Confidential Information is or was within the public domain, or obtained from a third party having lawful possession thereof, as the case may be, at the time such disclosure was made to Recipient.

(d) Recipient and its Representatives will not discuss any details of the Confidential Information with any third-party except as otherwise provided herein.

(e) Recipient agrees that neither the Discloser nor its agents shall have any liability to Recipient resulting from the use of the Confidential Information supplied hereunder, except that nothing herein shall waive any rights or obligations Recipient or Discloser or its agents may have with respect to the contents of the Confidential Information.

(f) Recipient acknowledges that it has been advised that the Property may be viewed by appointment only and Recipient specifically agrees that it shall not attempt to view, visit or otherwise gain access to the Property unless and until Discloser has scheduled an appointment for Recipient to do so.

2. Non-Circumvent

In consideration of Discloser’s disclosure of the Confidential Information, and without limiting anything else set forth herein, neither Recipient nor any of its Representatives shall at any time prior to the date immediately preceding the second (2nd) anniversary date of this Agreement, without the prior written consent of Discloser, which consent may be withheld by Discloser in its sole discretion, take any action, directly or indirectly, to undertake the Transaction including, without limitation, attempting in any manner, directly or indirectly, to contact a potential seller or any of its shareholders, officers, directors, or affiliates, introduced or revealed to Recipient by Discloser, to undertake or complete the Transaction.

3. Destruction/Return of Confidential Information

Recipient, upon the request of Discloser, will either (a) promptly destroy all copies of the written Confidential Information in Recipient’s and/or any Representative’s possession, including but not limited to written summaries of any oral analyses, compilations, studies, or other documents prepared by the Recipient or any Representative in connection with the Transaction or provided by Discloser, and confirm such destruction to Discloser in writing, or (b) promptly deliver to Discloser, at Recipient’s own expense, all copies of such written Confidential Information in Recipient’s and/or any Representative’s possession; provided that nothing herein shall require Recipient to produce particular documents or information that constitute attorney-client privilege or attorney work-product (however, Discloser expressly retains the right to challenge any designation of attorney-client privilege or attorney work-product). Any oral Confidential Information will continue to be subject to the terms of this Agreement.

4. Legal Disclosure

In the event that Recipient or its Representatives are requested pursuant to, or required by, applicable law, regulation or legal process to disclose any of the Confidential Information, Recipient will promptly notify Discloser, in writing, so that Discloser may seek a protective order or other appropriate remedy or, in Discloser’s sole discretion, waive compliance with the terms of this Agreement. Recipient will cooperate in Discloser’s efforts to obtain a protective order or other reasonable assurance that confidential treatment will be given to the Confidential Information and the existence of the Transaction or discussions between the Parties relating to the Transaction. In the event that no such protective order or other remedy is obtained, or that Discloser does not waive compliance with the terms of this Agreement, Recipient will furnish only that portion of the Confidential Information which Recipient has a duty as a matter of law to disclose, such determination to be made in good faith reliance on the written advice and direction of Recipient’s legal counsel.

5. Remedies

In the event of a breach or threatened breach by Recipient of the provisions of this Agreement, Recipient agrees that the remedy at law available to Discloser would be inadequate and that Discloser shall be entitled to seek an injunction, without the necessity of posting bond therefore, restraining Recipient from disclosing, in whole or in part, such Confidential Information. Nothing herein shall be construed as prohibiting Discloser from pursuing any other remedies, at law or in equity, in addition to the injunctive relief available under this Agreement, for such breach or threatened breach, including the recovery of consequential and punitive damages from Recipient. In addition, in the event of any violation of this Agreement by Recipient or its Representatives, Recipient shall reimburse the Discloser and its affiliates for all costs and expenses, including reasonable attorneys’ fees, incurred in order to enforce the provisions of this Agreement or exercise any remedies for a violation thereof.

6. Waiver

Recipient agrees that no failure or delay by Discloser in exercising any right, power or privilege hereunder will operate as a waiver thereof, nor will any single or partial exercise thereof preclude any other or further exercise thereof of the exercise of any right power or privilege hereunder.

7. Binding Agreement and Assignment

This Agreement shall be binding upon Recipient, its Representatives, its personal representatives, successors and assigns, and shall run to the benefit of Discloser and its affiliates, successors and assigns. This Agreement is not assignable by Recipient, and any attempted assignment by Recipient shall constitute a material breach by such party.

8. Severability

If any portion of this Agreement is held to be invalid or unenforceable for any reason, it is agreed that said invalidity or unenforceability shall not affect the other portions of this Agreement and that the remaining covenants, terms and conditions or valid portions thereof shall remain in full force and effect and any court of competent jurisdiction may so modify the objectionable provision as to make it valid, reasonable and enforceable.

9. Notice

Any notice or communication required or permitted to be given by any provision of this Agreement shall be deemed to have been effectively given and received on the date personally delivered to the party to whom it is directed or when deposited by registered or certified mail, with postage prepaid, and addressed as set forth on the signature page hereof. Either party may change its notice address by delivering a written change of address to the other party in the manner set forth in this paragraph.

10. Agency Disclosure

Broker as Single Agent or Transaction Agent. Broker has been retained by owner of the Property in the capacity of:

☐ Single Agent for Owner/Seller ⌧; Transaction Broker

For purposes of this agreement, a “Single Agent” means a broker who represents, as a fiduciary, either the purchaser (or lessee, as appropriate) or seller (or lessor, as appropriate) but not both in the same transaction.

For purposes of this agreement, a “Transaction Broker” means a broker who provides limited representation to a purchaser (or lessee, as appropriate), and seller (or lessor, as appropriate), or both, in a real estate transaction, but does not represent either in a fiduciary capacity or as a single agent. In a transaction broker relationship, a purchaser (or lessee, as appropriate) or seller (or lessor, as appropriate) is not responsible for the acts of a licensee. Additionally, the parties to a real estate transaction are giving up their rights to the undivided loyalty of a licensee. This aspect of limited representation allows a licensee to facilitate a real estate transaction by assisting both the purchaser and the seller, but a licensee will not work to represent one party to the detriment of the other party when acting as a transaction broker to both parties.

11. Applicable Law

This Agreement shall be governed by and construed in accordance with the laws of the State of Florida, without giving effect to the principles of conflict of laws thereof. Any action to enforce or construe the terms of this Agreement shall be brought in a state or federal court of competent jurisdiction in Florida.

12. Entire Agreement

This Agreement constitutes the entire agreement between the parties hereto with respect to the subject matter of this Agreement and supersedes and is in full substitution of any and all prior agreements and understandings whether written or oral between the parties relating to the subject matter of this Agreement. No modification, amendments or waiver of the terms and conditions hereof shall be binding upon Discloser, unless approved in writing by Discloser.

This Agreement may be executed in counterparts, each of which shall constitute an original, but all of which shall constitute one agreement. This Agreement may be executed by facsimile and PDF copy signature or other electronic means, which shall be accepted as if they were original execution signatures.

The following information from your profile will be used in the agreement:

Process. Execution. Results.